When someone passes away in Florida, their estate often has to go through a legal…

Planning for long-term care is becoming increasingly important as the cost of healthcare continues to rise. Many Americans worry about how they will pay for nursing home care, assisted living, or other long-term care services without losing their life savings.

The need for affordable long-term care services in America continues to grow. Costs can be extremely expensive, including long-term care insurance premiums, assisted living expenses, and monthly nursing home bills.

Key Takeaways: Medicaid and Long-Term Care Planning

- Medicare generally does not cover long-term nursing home care.

- Medicaid may help cover long-term care costs for individuals who meet financial and medical eligibility requirements.

- Owning a home does not automatically prevent someone from qualifying for Medicaid.

- Medicaid estate recovery rules may allow the state to recover certain costs after a recipient’s death.

- Early elder law planning can help families understand their options and protect assets.

How Many Americans Need Long-Term Care?

The U.S. Department of Health & Human Services (HHS) reports that Americans aged sixty-five and older have a 70 percent chance of requiring long-term care services during their lifetime.

Family members often absorb these costs for their loved ones. This can place significant pressure on their own financial security.

Because Medicare does not generally cover long-term care, many Americans turn to Medicaid as a potential solution for paying for care.

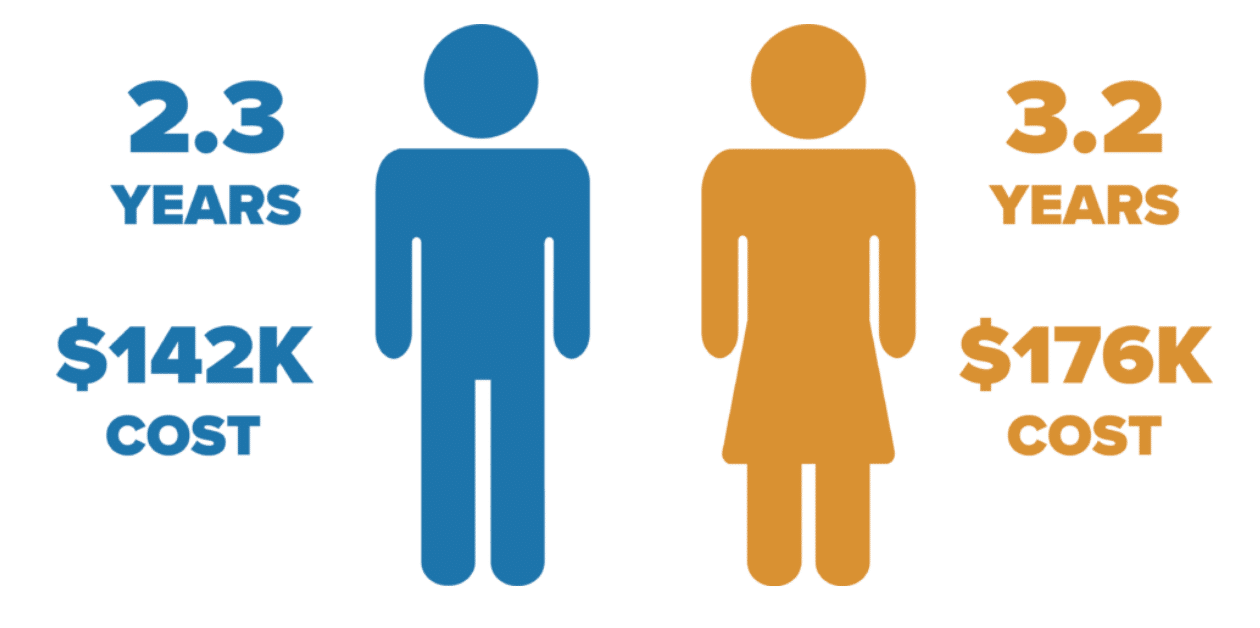

How Long Will People Need Long-Term Care?

A study by the Urban Institute, commissioned by HHS, found that Americans turning age 65 between 2020 and 2024 may require several years of long-term care.

| Group | Average Long-Term Care Needed |

|---|---|

| Men turning age 65 | Approximately 2.3 years |

| Women turning age 65 | Approximately 3.2 years |

Does Medicaid Pay for Long-Term Care?

Many people believe Medicaid coverage for long-term care only becomes available after a person has spent nearly all of their assets. However, Medicaid planning rules are more complex.

You do not automatically have to sell your home to qualify for Medicaid. However, this does not mean your home is always completely protected.

How Does Home Ownership Affect Medicaid Eligibility?

Medicaid generally does not count an applicant’s primary residence as an asset when determining eligibility if the applicant intends to return home.

However, states may have additional requirements, including limitations on home equity.

| Factor | How It May Affect Medicaid Planning |

|---|---|

| Primary residence | May be excluded if eligibility requirements are met. |

| Home equity | Must remain within applicable state limits. |

| Mortgage or secured debt | May reduce the home’s countable equity value. |

Home equity is generally calculated by subtracting secured debts, such as a mortgage or home equity loan, from the home’s fair market value.

When Can Medicaid Place a Lien on a Home?

Although a home may not need to be sold to qualify for Medicaid-funded long-term care, the state may place a lien on the property in certain situations.

Medicaid generally cannot place a lien if the applicant lives with:

- A spouse.

- A disabled or blind child under age twenty-one.

- A sibling who has an equity interest in the home.

What Is Medicaid Estate Recovery?

Medicaid estate recovery allows states to recover certain long-term care costs from the estate of a deceased Medicaid recipient.

The Omnibus Budget Reconciliation Act of 1993 requires states to recover certain costs from eligible estates, which may include home equity.

The goal of estate recovery is to help maintain Medicaid funding while continuing to provide healthcare assistance to individuals who cannot afford private long-term care.

Why Is Medicaid Planning Important?

The rising cost of long-term care means many families must consider how they will pay for future healthcare needs.

Even individuals who planned for retirement may struggle with the increasing cost of:

- Long-term care insurance premiums.

- Nursing home care.

- Assisted living facilities.

- Home healthcare services.

Because of these challenges, some families explore Medicaid planning strategies before care is needed.

Common Medicaid Planning Strategies May Include:

- Asset protection planning.

- Medicaid qualifying trusts.

- Long-term care planning.

- Estate planning strategies.

- Reviewing ownership of assets.

What Are the Current Challenges With Medicaid?

The Medicaid and CHIP Payment and Access Commission (MACPAC) has recommended changes to Medicaid estate recovery rules, including making recovery voluntary.

These proposals aim to address concerns about financial hardship. However, reducing estate recovery could also increase government spending and reduce funds available for Medicaid programs.

The Future of Medicaid and Long-Term Care Planning

America faces increasing challenges in funding long-term care. Families need solutions that allow seniors to receive necessary care while protecting their financial security.

The middle class needs options for paying for long-term care without having to significantly restructure finances or transfer assets simply to qualify for Medicaid.

Early planning allows families to better understand their options and make informed decisions about healthcare, assets, and future care needs.

Frequently Asked Questions About Medicaid and Long-Term Care

Does Medicaid pay for nursing home care?

Medicaid may cover nursing home care for individuals who meet specific financial and medical eligibility requirements.

Do I have to sell my home to qualify for Medicaid?

No. Owning a home does not automatically prevent someone from qualifying for Medicaid. However, home equity rules and estate recovery laws may apply.

When should I start Medicaid planning?

Medicaid planning is generally most effective when started before long-term care is immediately needed. An elder law attorney can explain available options based on your circumstances.

Speak With an Elder Law Attorney About Medicaid Planning

If you are concerned about paying for long-term care or protecting assets while planning for Medicaid eligibility, professional guidance can help you understand your options.

If you would like to discuss ways we can help, please contact our office at (352) 565-7737.